Contribution to recognized provident fund (‘RPF’) and/or approved superannuation fund (‘ASF’) are the most popular saving options being selected by the employees across the industries.

In addition to the above, it is very common that the employer makes payment to employee as gratuity. This is because, various tax deductions are available to the employer and the employee under the ITA[1] in respect of above payments.

In this article, we shall discuss the concept of RPF in detail from the perspective of ITA. Other two, namely ASF and Gratuity Fund will be covered in the subsequent parts.

Recognized Provident Fund:

The term RPF is defined under Section 2(38) to mean a provident fund which is recognized by the PCCIT/CCIT/PCIT/CIT in accordance with the rules contained in Part A of Fourth Schedule, and includes a provident fund established under a scheme framed under the EPF Act[2]. The procedure for obtaining registration has been provided in the rules contained in Part A of Fourth Schedule.

In other words, an employer may select provident fund framed under the EPF Act[3] or create its own provident fund and get it recognized by PCCIT/CCIT/PCIT/CIT. Among the two options, provident fund account framed under the EPF Act is widely used by the majority of employers.

In any case, both of them are called RPF for the purposes of provisions of ITA.

Tax Implications on contributions to RPF:

There are certain deductions/exemptions available in respect of contribution made to RPF. Let us proceed to understand tax implications on contribution made to RPF.

Employer’s Contribution to RPF:

As far as employer’s contribution to RPF is concerned, Section 36(1)(iv) states that contribution to RPF is to be allowed as deduction subject to limit as may be prescribed[4].

In addition to the provision of Section 36(1)(iv), it is required to analyse the provision of section 43B as well, to claim deduction in respect of the employer’s contribution to RPF.

Section 43B states that notwithstanding anything contained in other provisions of ITA, employer’s contribution to RPF shall be allowed deduction only if such contribution is paid to the respective RPF account within the due date specified for filing the return of income under section 139(1). If the amount is not paid within the due date but paid after such date, the deduction is allowed in the year in which such amount is paid to the RPF account.

The next aspect is taxability of employer’s contribution in the hands of the employee. In this regard, Section 17(1)(vi) states that employer’s contribution to RPF in excess of 12 percent of the salary is taxable as salary. For the purpose of this clause, salary includes basic and dearness allowance, if the terms of employment so provide, but excludes all other allowances and perquisites.

Further, section 17(2) deals with the perquisites. Section 17(2)(vii) states that aggregate contribution to provident fund, national pension scheme and/or approved superannuation fund in excess of Rs.7,50,000 shall be considered as perquisite and taxable accordingly.

In simple words, on one hand, employer’s contribution to RPF in excess of 12 percent of salary is considered as salary under section 17(1). On the other hand, aggregate contribution to three funds in excess of Rs.7,50,000 shall be considered as perquisite under section 17(2). Hence, the 12% of salary cannot exceed Rs 7,50,000/- to be out of the ambit of salary/perquisite.

More about section 17(2) will be discussed in the next part with examples/case studies.

Employee’s Contribution to RPF:

Though the employee makes contribution to RPF from his salary income, employer collects the contribution from the employee and remits the same to the provident account of the employee. As the employer is collecting the amount from the employee, in order to make sure that the amount is remitted to the account of the employee within a time, certain checks have been provided in the ITA.

Section 2(24) (x) of the ITA states that any amount received from the employee as a contribution to the provident fund shall be considered as income in the hands of the employer. However, once the amount is remitted to the employee’s PF account, such amount is allowed as deduction under section 36(1)(va).

However, unlike to the employer’s contribution, if the amount is not remitted to the RPF account within the due date under section 36(1)(va) then, such amount is permanently disallowed, and no deduction is allowed even if such amount is credited to the RPF account in the next year.

For the purpose of section 36(1) (va), due date has been defined to mean due date specified under the respective acts. However, certain High Courts have held that employer is eligible to claim deduction under section 36(1)(va) even though the amount is not remitted within the due date specified under respective act but before the due date for filing the return of income under section 139(1). High Courts have come to such a conclusion by taking recourse to the provisions of section 43B.

In order to provide clarification on the due date, section 36(1)(va) has been amended by the FA, 21[5] which states provisions of section 43B are not applicable for the purpose of determining the due date under section 36(1)(va). This amendment has been inserted by way of Explanation to section 36(1)(va). However, judicial fora have held that the amendment to section 36(1)(va) by way of Explanation is applicable prospectively and not retrospectively. This argument has initiated another line of litigation.

Recently, the Hon’ble Supreme Court (‘SC’) in the case of Checkmate Services (P.) Ltd[6] has held that the non-obstante clause would not in any manner absolve the employer’s obligation to deposit the amounts deducted by it from the employee’s income, unless the same is deposited on or before the due date as per the respective acts as given in section 36(1)(va).

SC also held that the leeway granted to assesses to allow deductions on deposits made beyond the due date, but before the date of filing the return, cannot be applicable in the case of amounts held in trust, as of the employees in the given case. They are deemed to be held as income of the employers only with the object of ensuring the timely deposit of the same as per the respective laws. Hence, if the employer fails to deposit the monies collected towards ESI and PF from its employees within the said time limits of respective acts, the eligibility to claim such sums as deduction is lost forever.

The next aspect would be tax implication in the hands of the employee in respect of employees’ contributions to RPF.

In this regard, section 80C states that employees are eligible to claim deduction up to an amount of Rs.1,50,000 while computing the taxable income for the year.

Tax implications on Interest earned on RPF:

In the above paras, taxability of contribution to RPF has been discussed. In this part, taxability of income earned (interest) on amount in the RPF would be discussed.

As far as interest accrued on employer’s contribution, Rule 6 to Part A of Fourth Schedule states that interest on RPF to the extent of 9.5% per annum is not taxable in hands of the employee as salary.

Further, before the amendment by the FA, 21[7], interest accrued on employee contributions is exempt in the hands of the employee.

However, through the FA, 21, provisions of section 10(12) have been amended to provide that interest accrued on employee contribution where such contributions is more than Rs. 2.5 lakhs is taxable in the hands of the employee (only such interest which accrued on a contribution in excess of Rs. 2.5 lakhs is taxable). Further, if there is no contribution by the employer to the RPF, the limit of Rs.2.5 lakhs has to be increased to Rs. 5 lakhs.

In this regard, for the purpose of computation of taxable interest, Rule 9D of the IT Rules[8] states that separate accounts within the PF account have to be maintained in respect of taxable contribution and non-taxable contributions from Financial Year 2021-22.

Tax Implications on Withdrawal from RPF:

Withdrawal of the amount from the RPF is not taxable in the hands of the employee subject to the following conditions:

- If employee rendered continuous service with his employer for a period of five years or more;

- If the service has been terminated by reason of the employee's ill-health, or by the contraction or discontinuance of the employer's business or other cause beyond the control of the employee;

- if, on the cessation of his employment, the employee obtains employment with any other employer, to the extent the accumulated balance due and becoming payable to him is transferred to his individual account in any recognized provident fund maintained by such other employer[9];

- If the entire balance standing to the credit of the employee is transferred to his account under a pension scheme referred to in section 80CCD.

If an employee does not satisfy the above conditions, contribution to such fund (both employer’s and employee’s) is considered as contribution to unrecognized provident fund and taxed accordingly.

In such a situation, employer contribution and interest accrued thereon are taxable without any limit as salary. Further, in respect of employee’s contribution, employee is not eligible to claim deduction under section 80C and interest accrued thereon is taxable as income from other sources.

Section 192A states that any person authorised to make payment under EPF to the employee, if such amount is not eligible for exemption by virtue of provisions conditioned in Ruel 8 of Part A of Fourth Schedule, is liable to deduct tax at source at the rate of 10 percent if such amount exceeds Rs.50,000/-. Further, if recipient does not provide PAN, tax is required to be deduct at MMR.

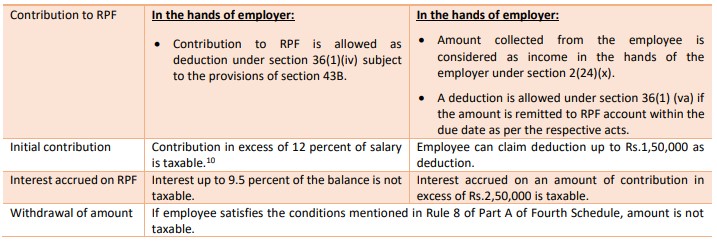

Summary of Taxability of Contributions to RPF

[1] Income Tax Act,1961

[2] Employees' Provident Funds and Miscellaneous Provisions Act, 1952

[3] Provisions of EPF Act are applicable if number of employees are 20 or more in any establishment.

[4] Limits on contribution has been provided in Rule 75 of Income Tax Rules,1962.

[5] Finance Act 2021

[6] [2022] 143 taxmann.com 178 (SC)

[7] Finance Act, 2021

[8] Income Tax Rules, 1962

[9] In the case, period of employment with the previous employer shall also be included for determining the 5 years continuous service condition.

[10] Aggregate contribution (RPF, NPS and ASF) in excess of Rs.7,50,000 is taxable as perquisites.